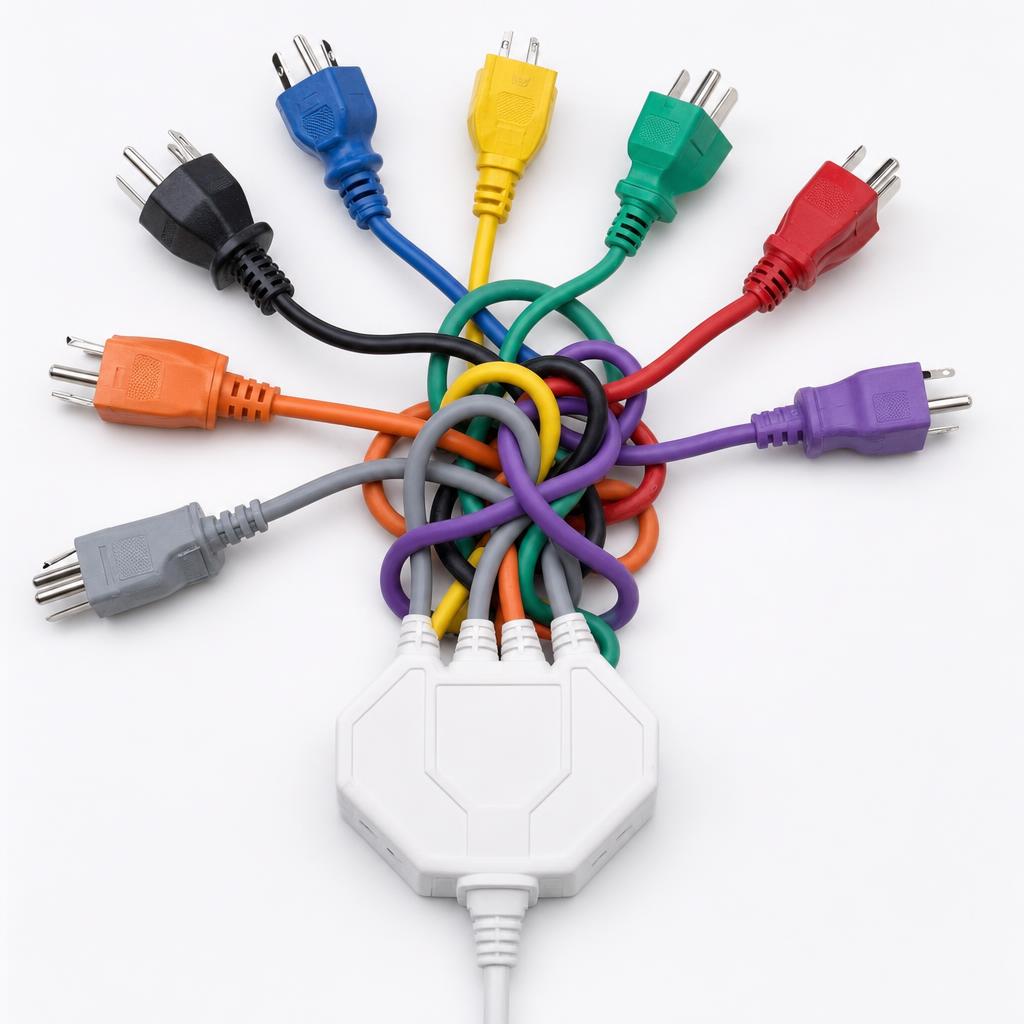

The average small and mid-sized business now subscribes to more than eight SaaS tools. Most of those tools were reasonable purchases when someone bought them — the best CRM on the market at the time, the most capable email platform, a solid HR system, a BI dashboard that impressed in the demo. Each renewed automatically. None of them talked to the others.

That is the state of SMB software in 2026: a landscape of subscriptions that individually make sense and collectively create a second job. Synchronising data between them is work nobody was hired to do. Managing training for each interface is a budget line nobody planned for. And somewhere between tool four and tool eight, the business stopped benefiting from software and started serving it.

A convergence is underway. The question is not whether consolidation is happening — the data makes that clear — but why it is accelerating right now, and which categories are being consumed first.

The Hidden Cost Nobody Calculated

When a company buys a SaaS subscription, it typically evaluates two numbers: the licence fee and the time required to get set up. These are the wrong numbers.

The real cost of each additional tool is what analysts have started calling the integration tax. Every new subscription that joins the stack creates a new data synchronisation problem. Customer records need to exist in the CRM and in the support platform and in the billing system. Order data needs to flow from the e-commerce layer into the ERP and from the ERP into the accounting software. When the same customer appears under slightly different names across three systems, nobody trusts any of them.

Recent research into SMB software costs found that companies running eight or more tools spend an average of 23% of their total software budget not on licences, but on the work required to connect those licences. That figure includes explicit costs like iPaaS subscriptions and API maintenance, but also the diffuse costs of staff time spent on manual imports, reconciliation, and the weekly task of checking whether the numbers in two systems agree with each other.

Training overhead compounds the problem. Every distinct interface a team member needs to navigate is a context switch. The average knowledge worker in a business running eight tools operates in at least four different interfaces daily. Context switching is well-documented as expensive: recovery time from a significant interruption runs to over twenty minutes. The cognitive cost of navigating incompatible UX paradigms — each system with its own logic for how records are structured, how dates are formatted, how searches work — is a continuous drag on output that never appears in a software budget line.

The third cost is harder to measure and often the most damaging: data silos. When customer data is distributed across eight systems, no single person has a complete picture of any customer relationship. Sales does not see open support tickets. Finance does not see the renewal risk score from the CRM. Operations does not see which customers are flagged as strategically important. Decisions get made on partial information, and the shortfall is rarely visible until its consequences are unavoidable.

Why 2026 Is Different

Consolidation has been discussed as a trend for years. What is different now is that the economics have shifted in three ways simultaneously.

First, unified platforms have closed the quality gap. For a long time, the argument for running eight best-of-breed tools was that consolidated alternatives were mediocre in most categories. That is less true than it was. The leading consolidated platforms in 2026 are genuinely competitive across CRM, finance, HR, and operations — not market-leading in every dimension, but close enough that the integration tax tips the calculation toward consolidation for the majority of SMBs.

Second, AI-powered business intelligence only works on connected data. The analytics capabilities that platform vendors are now shipping — natural language querying, automated anomaly detection, cross-domain forecasting — require a unified data model to function. If your sales data is in one system and your inventory data is in another, neither system can answer the question "which of our top customers are at risk because of our current stock levels?" A consolidated platform can. This is creating a pull toward consolidation that did not exist when BI meant simply running reports.

Third, the budget environment has made recurring software spend visible again. When money was cheap and growth metrics were king, eight tools at $200 per month each felt like rounding error. With tighter operational budgets and closer scrutiny on renewals, the $1,600 monthly tally — plus the integration overhead on top — is a number that gets discussed at the executive level.

What Gets Absorbed First

Not every software category is consolidating at the same rate. The clearest trend is CRM expanding outward. Modern CRM platforms have absorbed email marketing, marketing automation, and increasingly lightweight ERP functionality. The underlying logic is sound: the customer relationship is the centre of gravity for most business operations, and the tools that manage customer interactions are well-positioned to become the system of record for everything that touches a customer. Categories that once required dedicated point solutions — campaign management, lead scoring, pipeline forecasting — have become modules within platforms that were already doing half the work.

Business intelligence is the next category disappearing into the platform layer. Standalone BI tools required data to be extracted, transformed, and loaded into a warehouse — a pipeline that needed its own maintenance budget and specialist skills. Platforms with native BI eliminate that pipeline by making data queryable where it lives, which both reduces cost and dramatically shortens the time between a business question and an answer.

ERP is the slower-moving consolidation story, but it is moving. The traditional argument for dedicated ERP was depth — the ability to handle complex manufacturing runs, multi-entity accounting, or sophisticated inventory management that a CRM-first platform could not match. That argument still holds for large enterprises. For the SMB running a $5 million to $50 million operation, the depth gap has narrowed to the point where the integration benefits of a unified platform outweigh the feature premium of a specialist ERP.

For businesses trying to navigate which platforms have genuinely integrated their capabilities versus which are rebranding a collection of acquisitions under a unified login, resources like crmcompass.store publish structured comparisons that cut through vendor marketing — particularly useful when evaluating the CRM-plus-adjacent-modules question that sits at the centre of most consolidation decisions.

The Cost Comparison That Closes the Argument

A company running eight mid-market SaaS tools at average licence cost is typically spending between $1,400 and $2,200 per month on subscriptions alone. Add integration overhead — even conservatively estimated at 15% of that figure — and the true monthly cost of the stack sits above $1,600 at the low end. The leading consolidated platforms for SMBs covering the same functional scope price between $400 and $900 per month at comparable team sizes.

The arithmetic is not close. A consolidated platform at $700 per month, even accounting for migration costs amortised over 24 months, saves most SMBs between $8,000 and $18,000 annually in direct spend — before factoring in the productivity recovered from eliminating context switching, the data quality improvements from a single source of truth, and the time staff no longer spend on manual reconciliation between systems.

The consolidation case is not primarily about features. It is about total cost of ownership, data quality, and the compounding value of a system where every module was built to work with every other module from day one. The businesses that have moved have not gone back. The ones still evaluating are mostly waiting for a forcing function — a failed integration, a missed forecast, a new hire who asks why the company runs eight tools when one would do. In 2026, that question is getting harder to answer.